Palantir Gets One Fake Downgrade, One Real Upgrade

Palantir Gets One Fake Downgrade, One Real Upgrade

A Weird Day for Palantir..

Welcome back to DailyPalantir! Today, Palantir got a price target downgrade to $8.5 while also getting an upgrade to $29…let’s get into it!

Palantir Price Action

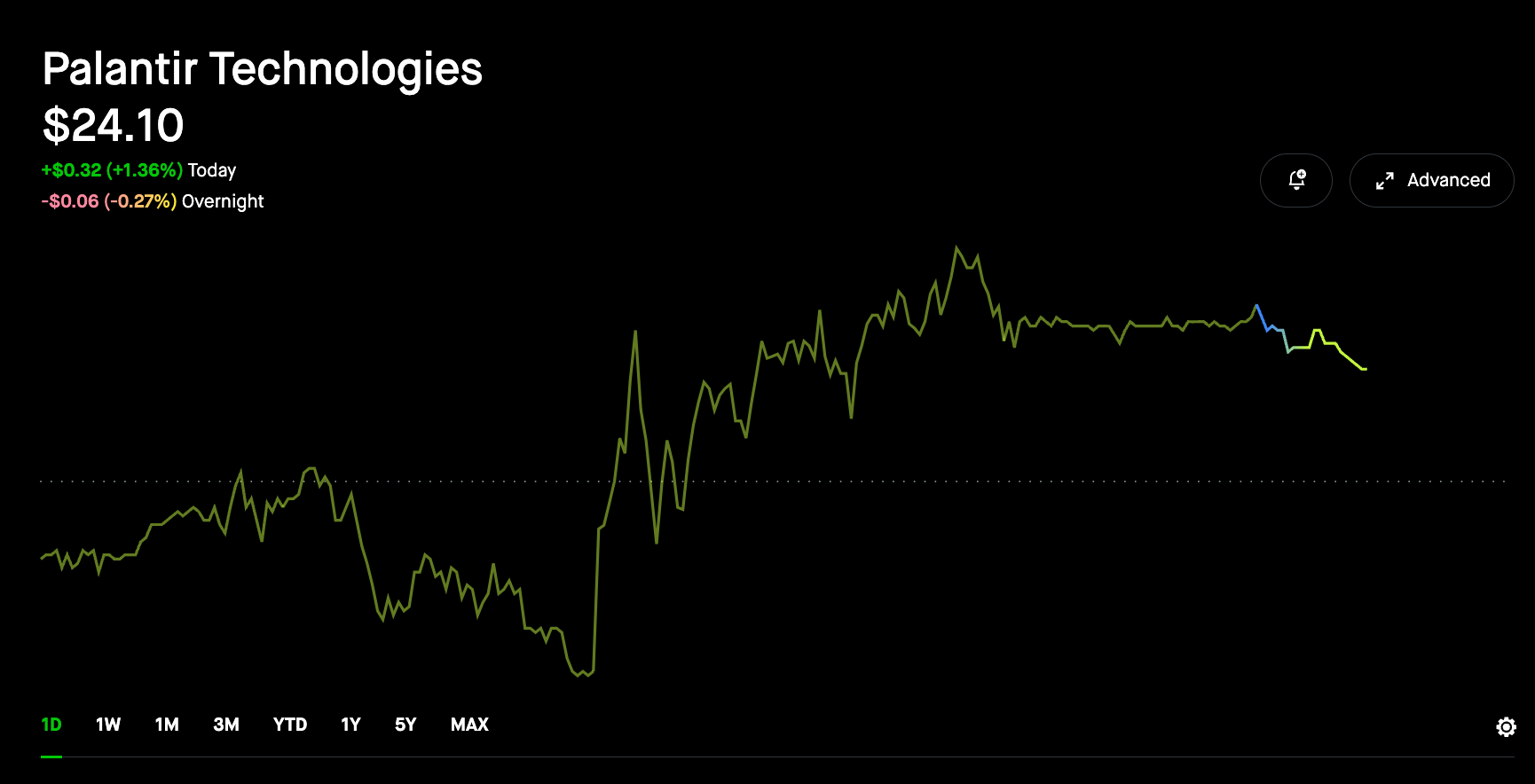

Palantir's stock had a good day, closing at $24.20 after hours, up 1.34%. This is interesting because big tech stocks like Nvidia and Snowflake were down. Nvidia dropped about 7% including after-hours trading, and Snowflake fell 2.35%. The fact that Palantir's stock went up while these other tech giants went down shows that investors are seeing something different and positive in Palantir.

One big reason for Palantir's rise is its unique position compared to other SaaS companies. While Snowflake and Salesforce, which also had a rough day, are more traditional, Palantir has a strong government business and is big in AI-driven defense technology. This makes it stand out. Even though Nvidia, a leader in AI infrastructure, had a bad day, Palantir's stock went up, showing that investors are recognizing its unique strengths and potential.

The overall market trends also helped Palantir. Investors seem to be spreading their money around more, looking beyond just big tech names like Nvidia. With small-cap stocks going up, it looks like there's a shift to other areas, including companies like Palantir. As more investors look for new opportunities, Palantir's strong government contracts and AI capabilities make it a good bet, and the market is showing that with Palantir continuing to gain momentum when traditional SaaS names are not in the current market.

The Fake Downgrade

So, we had something interesting happen today..

This downgraded ended up being fake, but it did make me think…

This downgrade seemed bizarre and didn't make much sense. UBS is a well-known financial institution, and such a drastic change in their price target was shocking. However, it turned out that this headline was fake, and UBS doesn't even cover Palantir. Someone had manipulated a headline to make it look real and spread it through the news wires. Whether there was real manipulation or not is yet to be known, but since UBS does not cover Palantir, it does feel like someone made it up.

The fake downgrade also didn't really affect Palantir's stock. Normally, a downgrade from a major institution like UBS would cause a noticeable drop in the stock price. But in this case, the stock didn't react much at all. This lack of reaction indicated that investors were skeptical of the news. If UBS had genuinely downgraded Palantir to such a low price, the market would have responded differently. The fact that the stock remained steady suggested that the downgrade was not taken seriously by the market.

Now why would someone do a fake downgrade? One theory is that someone wanted to manipulate Palantir's stock price to buy shares at a cheaper rate. By spreading false information about a major downgrade, they might have hoped to cause a sell-off, allowing them to purchase the stock at a lower price. This kind of market manipulation is concerning and highlights the need for investors to verify news from reliable sources — for a good two hours, most of us in the community felt this was real, until we finally realized, it’s fake.

If we did get to $8.5 again, Palantir would be a $20B market cap. Oh the things I’d do to buy at those prices again..

The Real Upgrade — Argus Research

Argus Research initiated coverage on Palantir with a $29 PT. Here’s the link to the full report.

Key takeaways:

They acknowledged that while Palantir has traditionally served U.S. defense and intelligence communities, its expansion into the commercial sector with advanced data management and analytics platforms is a significant growth driver. Argus sees the government business, which generated 55% of Palantir's revenue in 2023, continuing to grow, but the commercial business, especially in the U.S., is expected to be a major future growth area.

Argus highlights Palantir's reliance on new AI-powered applications to expand its business as a crucial aspect of their bullish outlook. They note that Palantir's shares are highly volatile and priced at a premium but emphasize that the company's highly differentiated software and unique capabilities justify this valuation. This cool factor and uniqueness set Palantir apart from other enterprise software companies, making it a compelling investment despite its premium price. If a Wall St firm can acknowledge that the company may be overvalued but still deserves the premium, then maybe it’s because they actually see the company as different from other enterprise SaaS players in a meaningful way.

Argus also appreciates Palantir's go-to-market strategy, which focuses on direct sales through account representatives and expanding its client base and wallet share within existing clients. They believe this approach suits the complex nature of Palantir's software solutions. The emphasis on boot camps and multi-day product seminars to demonstrate capabilities and educate clients is seen as a positive strategy. Argus notes that Palantir aims for long-term contracts, averaging 3.4 years, which adds stability and predictability to its revenue stream.

Argus also points out Palantir's impressive financial position, with $3.9 billion in cash and no debt, which provides a strong foundation for continued investment in research and development. This financial stability allows Palantir to invest heavily in R&D, running in the high teens as a percentage of revenue, well above many other tech companies. This is important because Palantir does not acquire companies, so they need to spend more internally on R&D in order to have a competitive edge and come out with new products consistently if they aren’t buying out smaller companies.

Argus believes that Palantir's ongoing investments in technology will drive long-term growth and further solidify its position as a leader in the AI and analytics space.

Risks:

The report acknowledges the risks associated with Palantir's business model, including client concentration, reliance on government contracts, and the inherent complexities of their projects. However, Argus believes these risks are balanced by the critical nature of Palantir's work for major clients like the U.S. Department of Defense and intelligence agencies. They highlight Palantir's strong ethical guidelines and its avoidance of business in China as positive factors that mitigate some of these risks.

Overall, Argus's upgrade to a $29 price target is based on Palantir's unique position in the market, its innovative AI applications, and its strong government and growing commercial business. They see significant potential for future growth, driven by Palantir's differentiated approach and strategic market position.

I think the research note makes sense. They acknowledged a strong government business, a go to market strategy with bootcamps, and potential overvaluation but AI tailwinds differentiating the company from its peers.

It definitely was more real than a $8.5 downgrade, haha.

Tomorrow I’ll go deeper into the $480M Maven Contract we got two weeks ago!

That’s it for today - see you tomorrow!

This newsletter will always be free and never have paywalled content. To support the newsletter, you can give a gift subscription below. Thank you for reading daily!

I would like to see:

A public retraction from MT

A public retraction from UBS

An investigation by the SEC

A retraction from all the companies that bought into the fake news: finviz.com, Charles Schwab (which still hadn’t removed from its webdite) and any others.

🫶🫶❤️❤️❤️