Palantir's Q1 Earnings Were Incredible

Palantir's Q1 Earnings Were Incredible

Even if the street didn't think so

HELLO EVERYBODY!

Sorry for the week of absence, for those keeping up on X/YouTube, it’s been a wild week, but I am officially back.

Last week I had the privilege of attending the SCSP AI Expo, where Palantir was the lead sponsor, and this ended up happening…

It was a pretty incredible moment. I’ll tell the story of how it all went down later in this newsletter, but we also got the chance to do this…

So last week was a real special week. Palantir invited Arny and I to the SCSP AI Expo, where Palantir was a leading sponsor. As a result of being there, we got to meet Palantir CEO, Alex Karp, and also record a 20 minute podcast with Palantir CTO, Shyam Sankar.

I’ll talk more about the podcast tomorrow, but here is the link for anyone who wants to see.

Meeting Dr. Karp was one of the coolest experiences in my life. He was on stage waiting for his panel to start in a very large room (I didn’t even think I’d be able to get in the room but I ended up getting a front row seat) and when he sits down, he locks eyes with me and then starts to wave. I wave back, confused that he actually knew me, but so grateful he did.

After his talk, he walked right up to me…

It was a really magical moment and I am so grateful to have had it. Dr. Karp was exactly how you see him on stage — authentic, funny, and filled with energy; the entire room could feel him when he spoke.

Special shoutout to Eliano and Chad, two Palantir employees, for making this happen.

Getting Into Q1 Earnings…

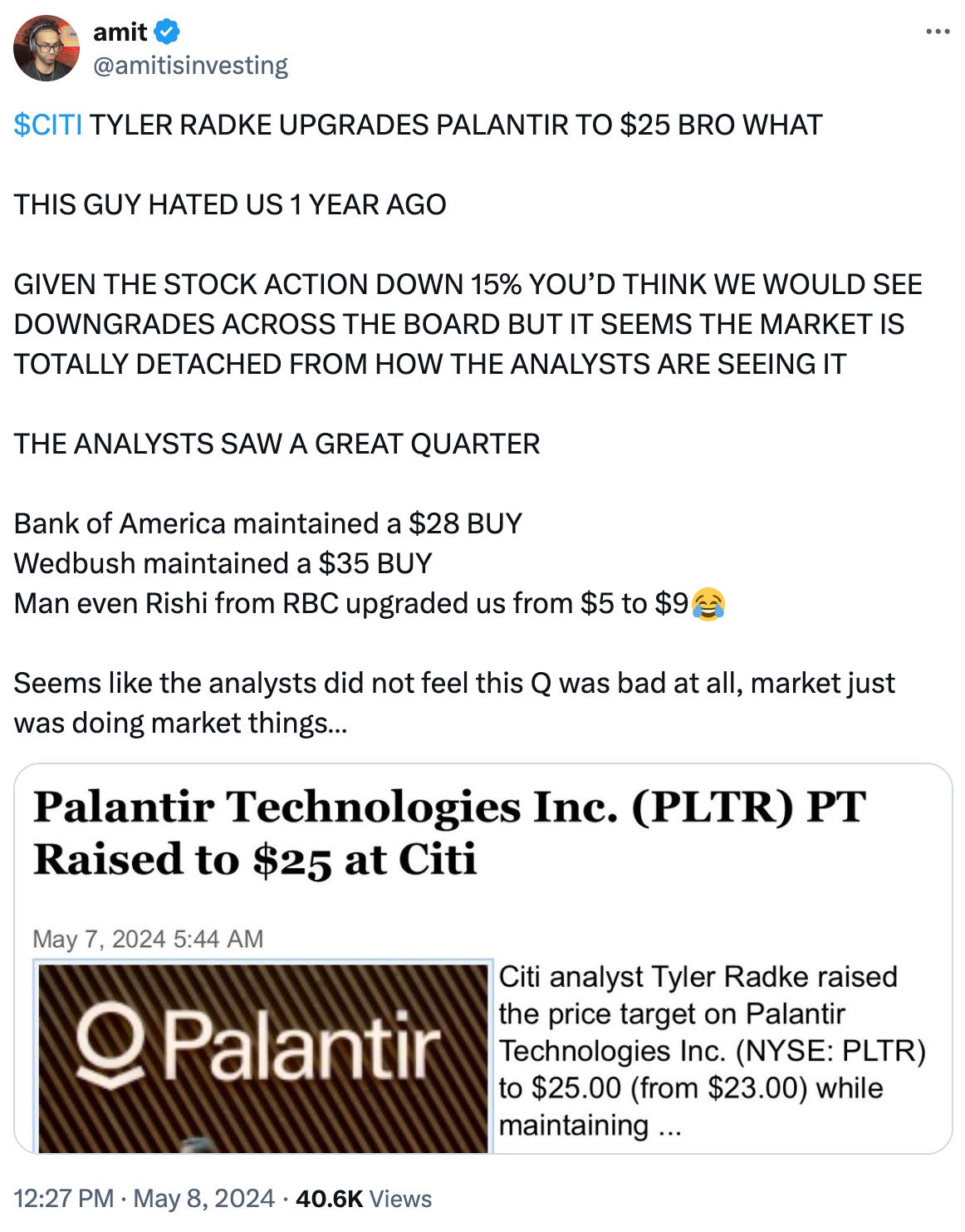

I thought Q1 earnings went very well. I know the stock hasn’t reflected that, but I believe that’s mainly because on earnings day, Palantir was up 10% at $25.36.

Usually when a stock moons right before earnings, expectations get so high, it’s hard to live up to it. If Palantir was 20 on earnings day, I could have easily seen the numbers we put up getting us to 23. Since we were 25, if numbers didn’t meet even higher expectations, the stock would sell off.

Now, although the stock hasn’t matched the numbers we saw…the analysts felt differently:

Almost every analyst covering Palantir upgraded the stock. Why?

It seems like the growth they put up more than justified the upgrades even if the market felt it ran up too much before earnings.

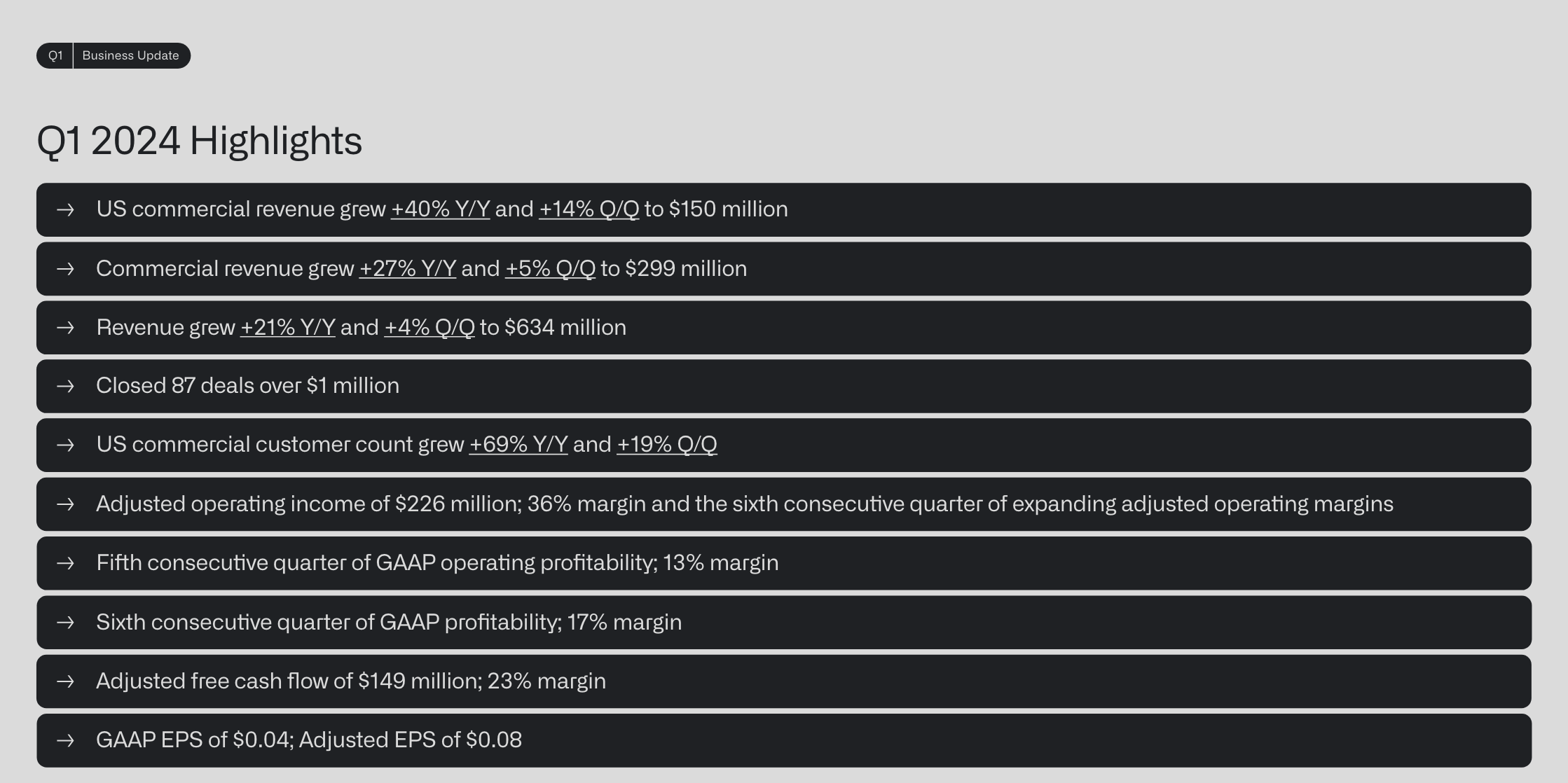

Highlights:

While many of the numbers are impressive, there’s 3 that stood out to me:

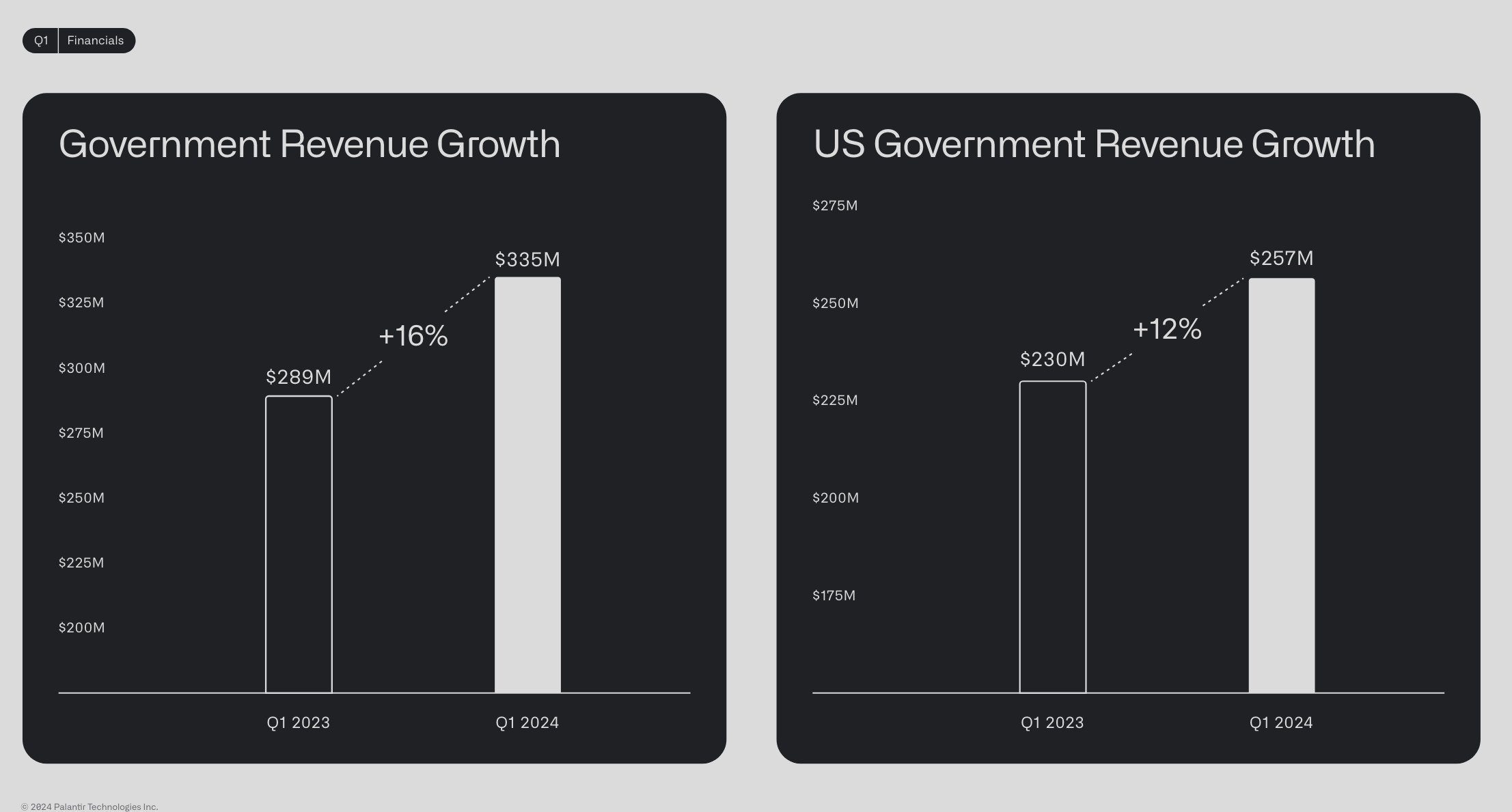

Government Revenue

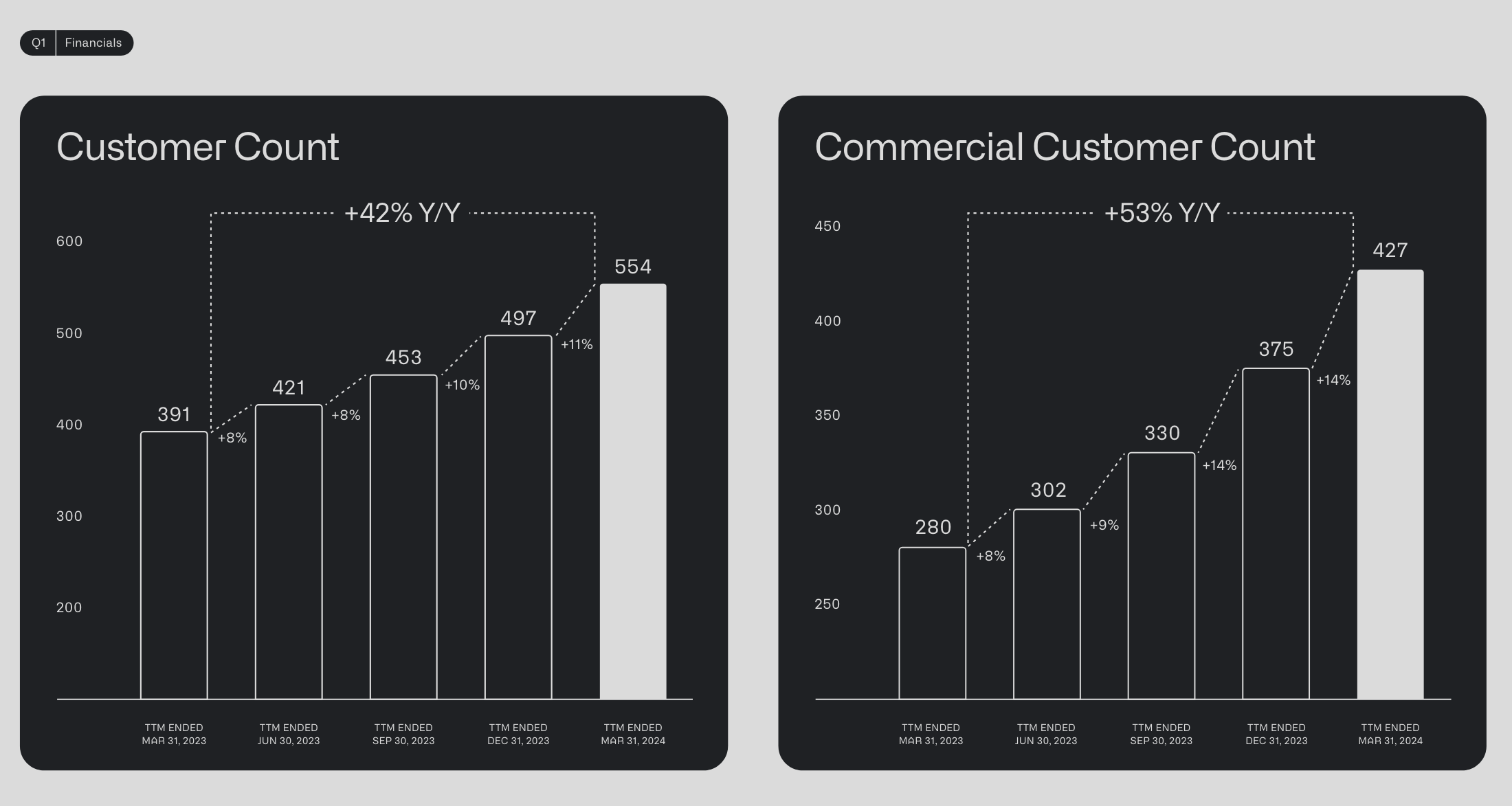

Customer Count

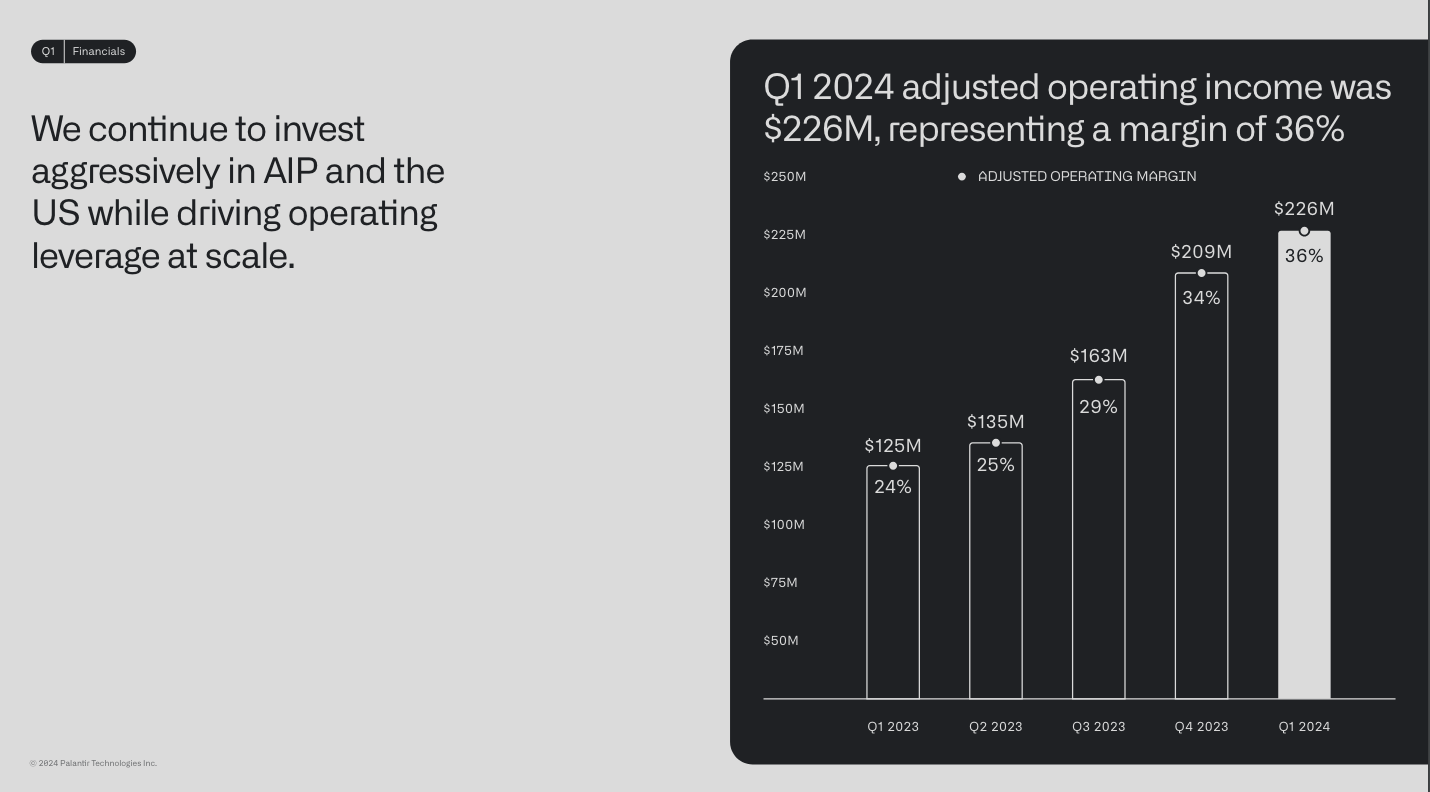

Adjusted Operating Income Margins

First, Government Revenue reaccelerated. We had seen declining gov revenues for the past few quarters, but in Q1, that changed:

We went from 11% growth to 16%, which is not bad at all. The international deals we closed along with TITAN were key catalysts. It also proves Palantir’s argument that the government business is lumpy, and some quarters show more growth than others. As FedStart continues to evolve as a product, we can expect more catalysts for Palantir to find government contracts even if they aren’t the direct beneficiaries of those deals.

Second, Customer Count continued to go higher:

We added 57 net new customers in the quarter, which means from the 660 bootcamps that were done, that’s about a 10% conversion rate (if every customer came from a bootcamp.) This is a big, big deal.

Palantir was a company that didn’t even know how to sell 2 years ago. I mean honestly, the company was partnering with SPACs just to be able to get clients. Bootcamps have been an absolute game changer and have fundamentally changed Palantir’s GTM — it’s also working! 42% YOY customer count is now joke and if we can continue to keep having that metric go higher, topline revenue growth (which is now ABOVE 20% at 21% YOY and came in with a 19M beat) will also go higher as well. US Commercial revenue came in at 40% YOY which was guided for last quarter, but Palantir raised that guidance to 45%, which seems to show that commercial customers in the US really are starting to buy from Palantir.

Finally, adjusted operating margins somehow went up.

This was a number that was at 17% 18 months ago…they increased it 5% QoQ during the last earnings, I really didn’t expect them to get even more efficient, but it speaks to how strong Palantir’s actual business is becoming.

If this number can get closer to 40% by the end of the year and we can continue to grow topline revenue closer to 25%, then the street absolutely will be able to justify the current valuation with a premium — the question simply becomes how quickly Palantir will be able to show they are growing customers in order for the street to feel the revenue will catch up. Customer count and adjusted margins going up shows that the business internally is getting much stronger, the revenue will follow, but these are good metrics to show that they are on the way.

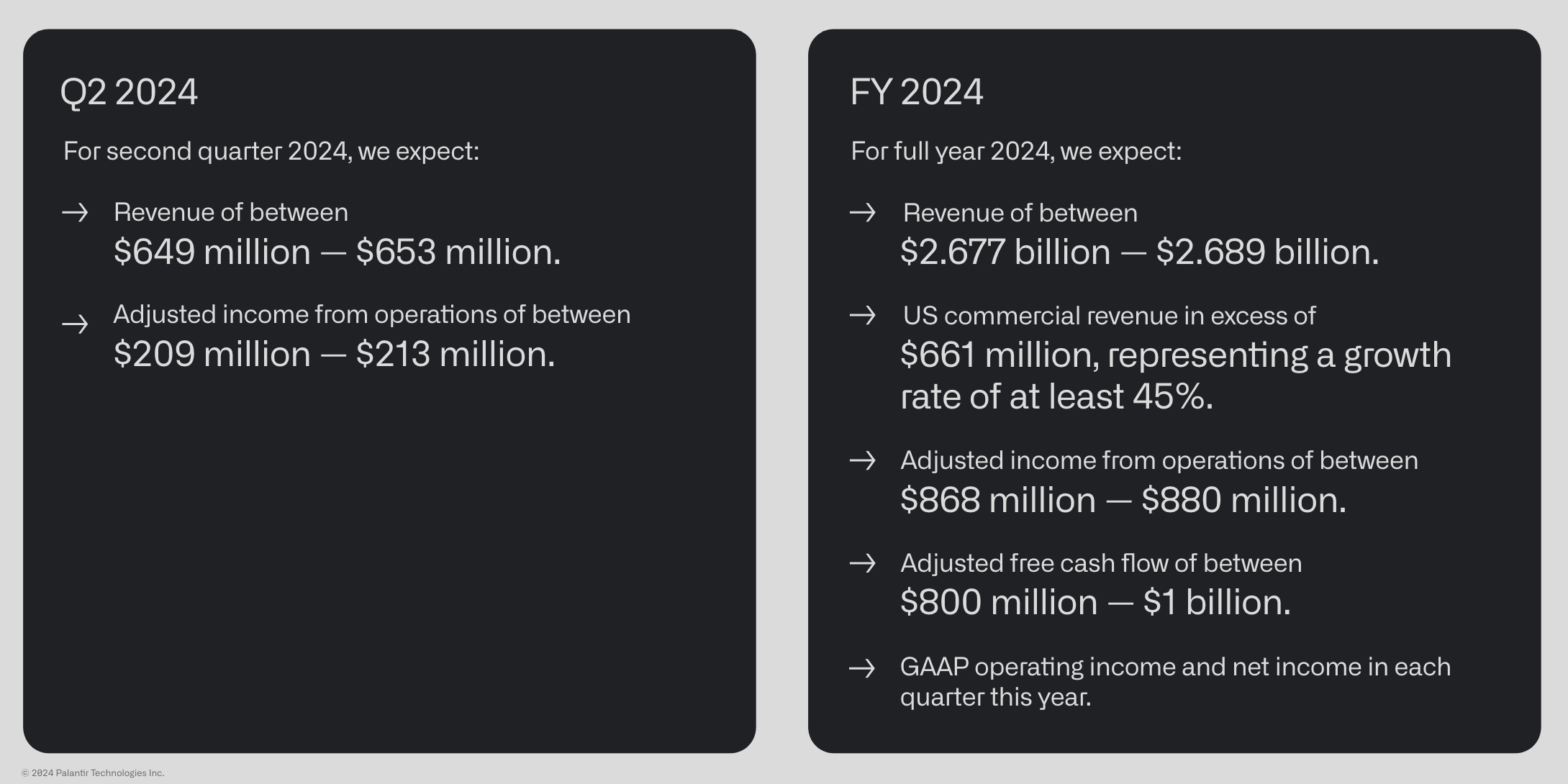

Full guidance increase from Palantir:

Overall, I just didn’t see any red flags to be overly concerned about. If I did, I would point them out, and if I’m missing any, please do respond and let me know. Even stock based compensation came in below 20% of revenues for the first time in 4 years.

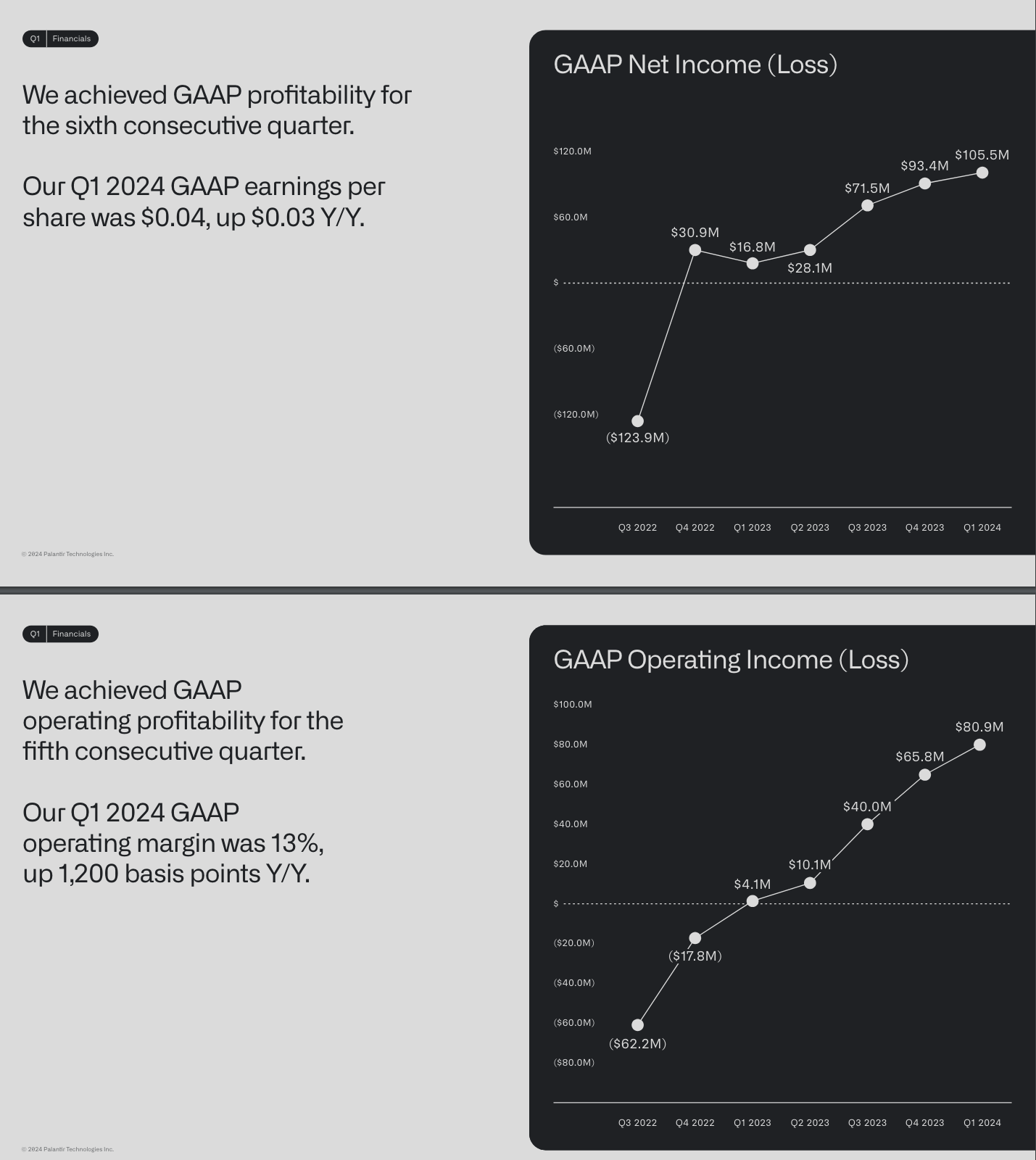

On top of all of this growth, with the highest interest rates in 40 years, Palantir continues to be GAAP profitable:

I saw a business that is exploding on customer count, proving their software is valuable to clients, and beginning the early phases of monetizing all those customers to eventually become Palantir customers for a very long time.

The company is executing on all fronts — and that’s what really matters to me.

That’s it for today - see you tomorrow!

This newsletter will always be free and never have paywalled content. To support the newsletter, you can give a gift subscription below. Thank you for reading daily!

PLTR’s 10K is the most impressive I have read in 60 years. All the risks are laid out on the table for everyone to see, in exquisite detail. All the numbers are conservative. There is no sales hype. As usual, past performance is no guarantee of future results. Nevertheless, one must pay attention to the track record. A company that can put $5 Billion in the bank, has no debt, has access to an unused line of credit for unforeseen opportunities, has multiple high profit margin product lines, and a dedicated research staff to keep the company in front of its competitors is beyond impressive.

Palentir’s only headwinds are short sellers, your anti-semitic types, your anti-American psychopaths and all those who don’t have anything good to say about anyone.

Don’t sweat the volatility. Don’t believe that your wishful thinking constitutes reality. Invest for your old age and for your children’s inheritance. Invest for your own security and independence. Don’t even fantasize about what you could do with your winnings…that’s what gamblers do.

Party On🥳🥳