Answering The Biggest Retail Palantir Q1 Questions

how is retail thinking about the future of Palantir?

Welcome back to DailyPalantir! In today’s newsletter, we’re going to discuss the top-voted questions asked by retail shareholders around Palantir for their upcoming Q1 earnings call. Let’s get into it!

Top Voted Questions

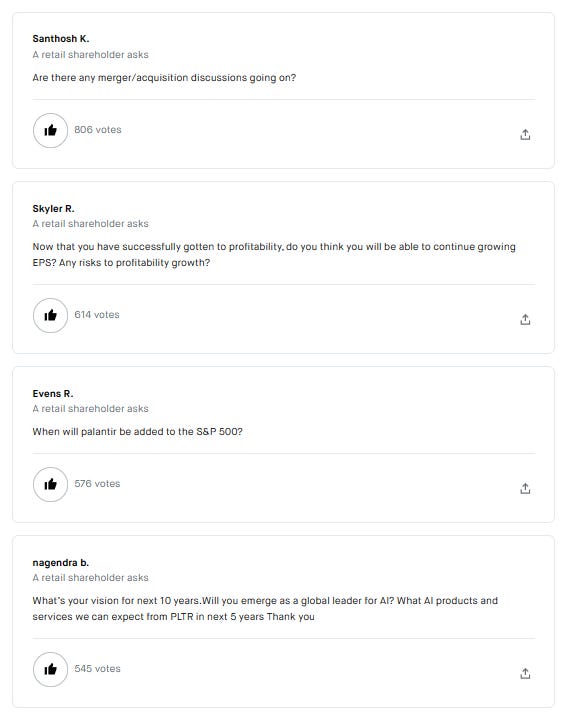

Here are the top voted questions by retail investors, you can ask a question using a Say Technologies, where all the questions are crowdsourced.

My Answers

Here’s how I would approach and answer these questions:

On Palantir providing services to Tesla:

While this is a good question, and I would personally love to see Palantir and Tesla working together — they probably can’t answer this even if they did have a partnership. Tesla is vertically integrated across their entire business so I’m not sure they would need Foundry/AIP to be an operating system for their data, but I definitely don’t think it could hurt. The one link we have between the two companies is that Palantir has a very close relationship with Panasonic Energy of North America and is the digital backbone for their Nevada factory — the same one providing batteries for Tesla.

On Palantir paying a dividend:

This is something I personally would not want Palantir to do. It just doesn’t make sense at this stage in the business to actually pay a dividend given the company needs to grow. The capital appreciation of the stock should be a reason to own it, not a dividend. I think many retail investors get confused when asking this question because a dividend is showing that a company can’t organically grow like it used to, therefore, it has to give shareholders a reason to stay. Apple just increased their quarterly dividend yesterday from 24 cents to 25 cents, which is great for shareholders, but you also have to ask yourself why they are doing this — the answer is because their revenues are down 5% YOY.

We want Palantir to be a company that can compound revenues at closer to 25% YOY so paying a dividend would be taking money away from their operations and into the hands of shareholders when they actually need that money to continue growing, hopefully to the 25% YOY number we all are looking for.

On Palantir’s Oracle partnership:

This is actually one of the most important questions that I hope we get some clarity on. We really don’t know much about this deal besides the PR, and I think it is going to be one of the most unique partnerships Palantir ever will do because Oracle tends not to do these types of deals, ever.

I’ve heard from multiple ex oracle employees that them deciding to have an explicit agreement with Palantir really mattered, and it was one of the deals the street got excited about for a day but then moved on from. I think it is a game changer and hopefully we can get more updates from it.

From the PR of the deal:

“Oracle is the only hyperscaler capable of delivering its entire AI and cloud suite to any business or government anywhere in the world,” said Rand Waldron, vice president, Oracle. “By combining the performance, scalability, and flexibility of Oracle Cloud Infrastructure with Palantir’s leading data and AI platforms, we will help our customers win in any industry or environment.”

“Palantir and Oracle are both dedicated to defending western interests and institutions around the world," said Josh Harris, executive vice-president, Palantir. “Oracle Cloud Infrastructure’s unique ability to help customers meet their regulatory, performance, and security needs will increase our impact and help our global clients gain the full benefits of cloud and AI.”

In any region, including commercial, sovereign, and government air-gapped environments, Oracle Cloud provides more than 100 cloud services and applications, including the latest innovation in generative AI, running on a blazing fast AI infrastructure. Oracle Cloud Infrastructure services and pricing are consistent across deployment types to simplify planning, portability, and management.”

On Palantir’s share buybacks:

This is another part of Palantir’s story that I feel many investors get wrong. Palantir has authorized $1B in share buybacks. It makes no sense, at all, to actually use that $1B at these levels.

Why?

Let’s say they bought back $1B worth of stock at $22.50. This would take 44M shares off the float of a company that has…2.1B shares outstanding.

Would it have an effect on shareholders and allow us to own more of the company? Yes.

Would that money have been better spent going into R&D, bootcamps, or just bonds to generate 5% so that we can continue to be GAAP profitable? I believe so.

I just don’t think doing a substantial buyback or issuing a dividend at these levels makes sense because Palantir is still trying to grow as a company and if they want to grow, they need their cash pile to do more for them then try to appease shareholders. The best way to make shareholders happy is to continue to grow, and if they can do that, they likely won’t need to buyback stock until they can buyback billions of dollars of stock over the next decade like the current big tech companies that can do it today.

On Palantir’s AI Strategy:

This would best be answered with bootcamps. The Bloomberg article on Palantir’s bootcamp strategy was pretty incredible — the article really did go in depth around what Palantir is doing when it comes to sales and how they are partnering with organizations across the world.

Palantir has averaged 5 bootcamps a day in 2024. If the conversion on those are even 10%, then their customer count should go much higher. This is crucial for their AI strategy because it is not about making money off these clients right now, it is about getting them into their ecosystem and being so sticky that these clients would never want to use any other AI product because of how strong Palantir’s is.

As a result, net dollar retention should increase, and Palantir should benefit in their long term as they keep those clients for years using their software.

On Palantir’s S&P 500 Inclusion:

We don’t know when this will happen but hopefully it will be on the next rebalance. I am hopeful but skeptical. If anything, I do think 2025 will be the year.

The main reason I believe the committee did not select them last time is because Palantir would have the second lowest level of institutional investors out of all 500 companies in the S&P. Because the S&P wants companies that are not as volatile and have a stable investor base, they may wait for this number to go higher. Right now, its 40% institutional and 60% retail. If that flips in the next year, I think we may see them included. We also may join simply because the committee wants the index to have more AI exposure, so if Palantir continues to show they are a pure play AI name, that may be a catalyst even with low institutional ownership to get into the index. Every other requirement has been met to join.

On Palantir’s risks to profitable growth:

I think the main risk here is if adjusted operating income margins decline or customer count decreases QoQ.

As long as those two stay stable and grow, Palantir’s GAAP profitability should not be in question. This is another reason I like that they have $4B in treasuries, they will generate net interest income no matter what which will enable their profitability, now it is just a question on how fast can they grow their profitability, but it is unlikely they go back to not being profitable.

On Palantir M&A:

Karp has already said the company is not for sale. I highly doubt there would be a way to change his mind, especially since he just said this today….

“When we meet again in 10 years, I think we will be 10 to 20 times bigger.” — Palantir CEO, Alex Karp 10 times bigger would put $PLTR Palantir at a $500B market cap, 20 times would be a $1T market cap.

So, Palantir likely isn’t up for sale. In terms of doing an acquisition, Palantir hasn’t done one since 2016. They have constantly found a way to innovate internally, so I don’t expect them to acquire anytime soon, especially because since they also have the best talent in the world.

On Palantir’s 10-year vision:

The 10 vision should be to capture the market. It seems like Palantir is executing against that thesis.

I’ll have some more coverage coming this weekend going into Q1 earnings on Monday.

That’s it for today - see you tomorrow!

This newsletter will always be free and never have paywalled content. To support the newsletter, you can give a gift subscription below. Thank you for reading daily!